Reasons to Fade Inflation Fears: Daily Contrarian, Feb. 10

The CPI brings fresh inflation data this morning, but investors may have moved on already.

Good morning contrarians!

Listen to the podcast here or click the image below. You can also get it on Spotify (sorry, have to go to an outside link as Substack seems unable or unwilling to fix the upload issue they’ve been having).

Yesterday saw a big rally on Wall Street. Positive earnings news buoyed markets and tech stocks saw the best of it with the Nasdaq up 2%. In the after-hours, positive earnings results from Disney (DIS), Uber (UBER), MGM Resorts (MGM), Mattel (MAT) kept the party going.

It’s not just earnings that are driving this. We’ve also seen a quiet reopening rally as countries, states, and municipalities rolled back mask mandates and travel restrictions. Some of the biggest movers have been travel stocks. The Jets ETF (JETS) that tracks U.S. airlines is up 7% over the last week. Airbnb (ABNB) 8%. Hyatt Hotels (H) and Hilton (HLT) 6% each.

State of Play

Stock futures are mixed as of 0630. The Nasdaq is down about 0.3% while Dow Industrials are up 0.1%. S&P 500 and Russell 2000 are down about 0.2%.

Bonds aren’t really doing much. The 2-year yield is up a tick, to 1.35%. Ten-year up a tiny bit as well, to 1.94%.

Commodities are seeing some bids, with WTI crude oil up 1% to trade near $91/barrel. Industrial metals are rallying: Copper is up 2%, aluminium close to 3%, zinc and nickel almost 4%.

Cryptos are seeing muted gains, with bitcoin up 3% to trade around $44,800.

Inflation Watch, Redux

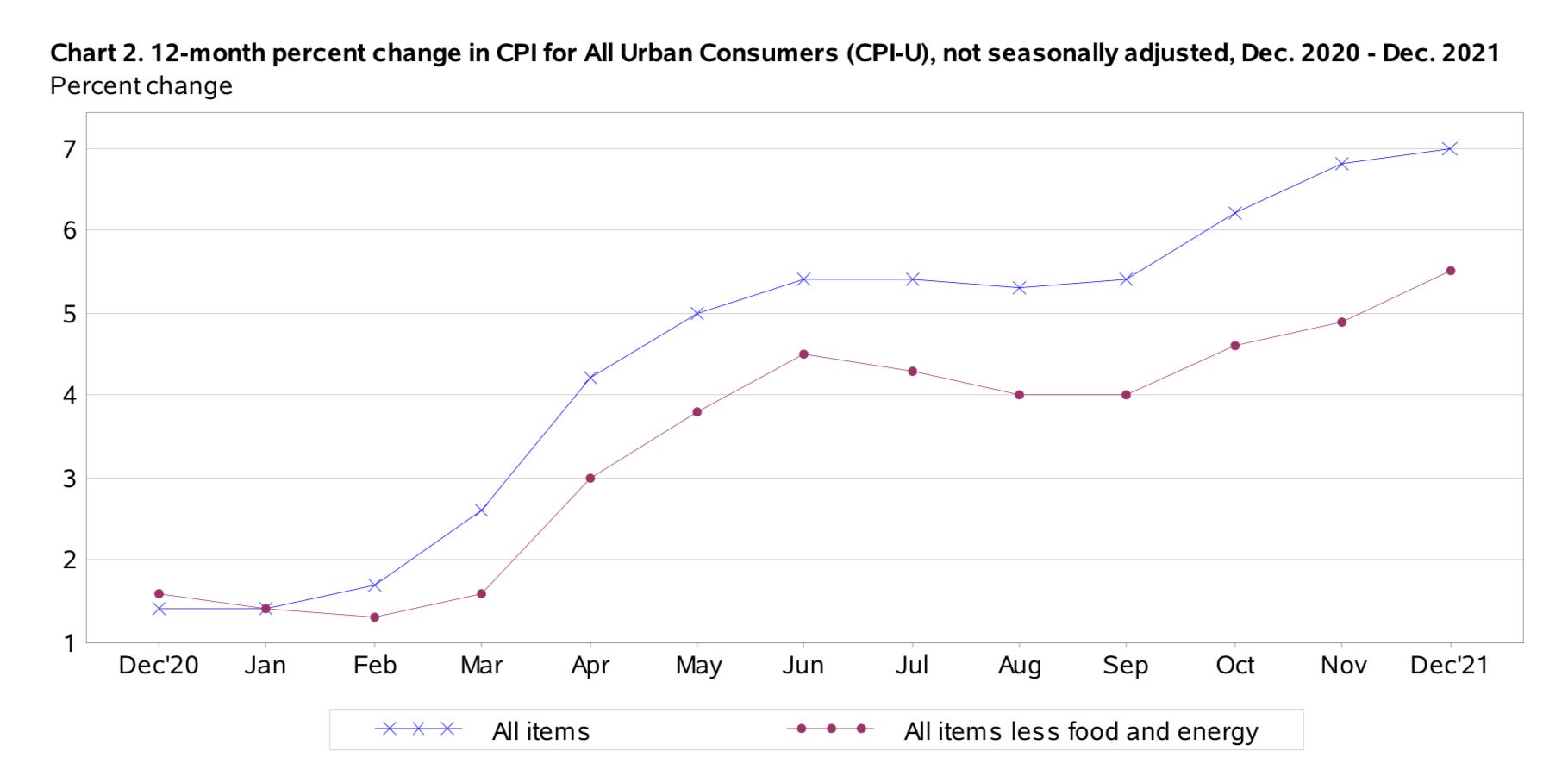

The focus returns to inflation today, with the Consumer Price Index from the Bureau of Labor Statistics due at 0830. Economists expect the CPI to have increased 7.3% year-over-year in January after 7% growth in December. The core figure, excluding food and energy, is expected to come in at 5.9% versus 5.5% last month.

These are heady figures and it makes sense for the Fed and investors to be concerned about inflation. Higher interest rates can cure inflation, but they can also choke off growth. Then there’s the question of how much to raise interest rates, how quickly, and how many times.

Fed fund futures are predicting five rate hikes this year. Some Wall Street banks are anticipating as many as seven, one at every FOMC meeting. If today’s CPI comes in hot, the concerns may even materialize for a rate increase of 0.5% or more at the Fed’s next meeting in March. Talk will intensify that the Fed was asleep at the wheel last year and hopelessly out of touch with their transitory talk. All of that would be bad for stocks. Presumably we would see the gains from the last couple of days evaporate.

That’s the conventional playbook. The contrarian take is that markets are already pricing in rate hikes and that the Fed doesn’t have the cojones to raise rates too aggressively too quickly. More on that in the bottom line.

We also have initial jobless claims out at the same time as the CPI report. Expect that to get overshadowed today but for what it’s worth, economists expect 230,000 new claims, roughly in line with last week’s number.

Earnings

Don’t forget about earnings. Still several of these to watch.

PepsiCo (PEP) just reported. The EPS was roughly in line with estimates but revenues topped forecasts and the company announced a new buyback campaign worth $10 billion and increased its dividend. Pepsi did warn of cost pressures though, so that might keep a bit of a lid on any gains. The stock is up about 1% in the pre-market at the time of this writing.

Credit Suisse (CS) just reported a worse-than-expected loss and had a lousy outlook, so that stock is down close to 5% this morning.

Duke Energy (DUK) and Philip Morris (PM) are up at 0700, followed by Kellogg (K), Coca Cola (KO), and PG&E (PCG) before the open at 0930. Also Twitter (TWTR) is due to report this morning. Zillow (ZG), Affirm (AFRM), and Expedia (EXPE) follow after the close at 1600.

Update: follow the Twitter to get the more timely pre-market earnings report card.

The Bottom Line©

Expect lots of noise about the CPI but it could come and go pretty quick.

Remember that a lot of this is trivial as this is just one report. There will be another, along with the PCE reading, before the Fed’s next meeting. In a few months we’ll no longer have the low ‘base effects’ from a year ago, so the more shocking inflation numbers should dissipate regardless.

And of course don’t forget the contrarian take, that this is all priced in already and the market is done being spooked about inflation or the Fed. The last couple of days (yesterday in particular) seem to demonstrate some more serious risk appetite. It’s entirely possible this whole thing turns into a non-event even if it does exceed expectations.

A final point: The CPI very rarely deviates from expectations. This is one data release the economists actually get right most of the time. Over the last five years, there have only been three times that the YoY core CPI has missed the survey number by 0.3 percentage points or more: May, June, and July of 2021. So if this thing does miss today, chances are it won’t be by very much.

Yesterday’s Bottom Line told you it was difficult to see where a catalyst for selling could materialize. Indeed, stocks rallied as they tend to do in bull markets. Are you convinced we’re still in a bull market? Good, because that might get tested again soon.