Good morning contrarians!

Stock futures are down a bit as of 0640, having recovered from earlier in the session. Small caps are seeing most of the selling, with the Russell 2000 down 0.8%. The Nasdaq is down 0.3% while S&P 500 and Dow Industrials hover closer to the break-even point. Bonds are selling off as well, with the yield on the 10-year up to 1.63%. The 2-year yield was up past 0.64% earlier, but is now down to 0.63%, still much higher than it was last week when it touched 0.45%.

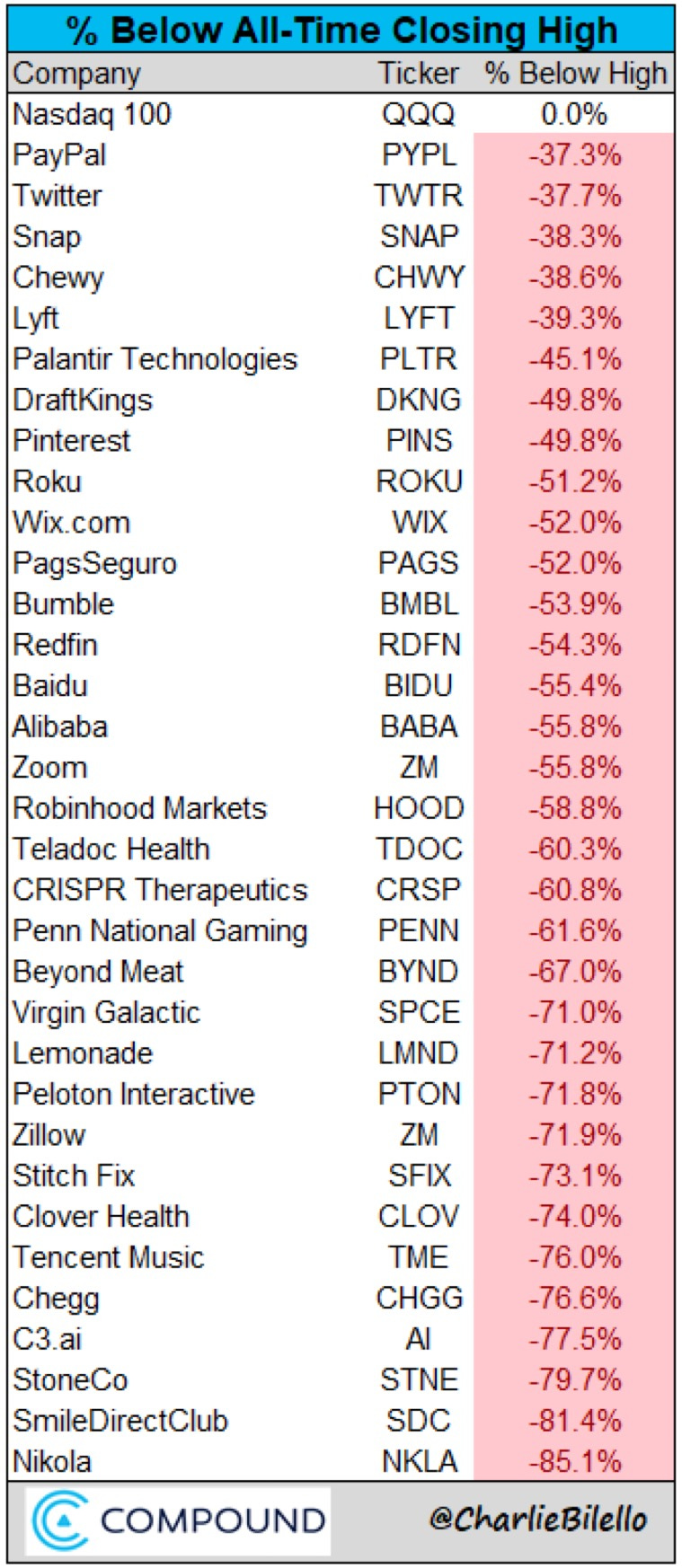

It is a time of competing narratives in markets that is worth attempting to unpack: Stocks have been beset by strange patterns dating back to last week, with lots of bifurcation. The bloom appears to be well and truly off the rose for some pandemic favorites: Peloton (PTON), DocuSign (DOCU), DoorDash (DASH), Snowflake (SNOW), CrowdStrike (CRWD) have all seen massive losses. Many are well into correction territory already.

The following table courtesy of Alpha Investors’ Twitter feed. They have their own substack you can subscribe to as well.

At the same time, the reopening trade has not really resumed. Covid concerns are rising again, especially in Europe where some countries are going back into lockdown. Travel stocks have done poorly as well.

There are other issues at hand. Payment stocks are selling off, led by Paypal, which is down to a 52-week low. Visa (V), Mastercard (MA), American Express (AXP), and Square (SQ) are all seeing heavy selling. This appears to be due to regulatory concerns with one analyst calling this a ‘perfect storm’ for the sector.

Energy names were one bright spot yesterday but it bears watching how this rotation (or whatever it is) will unfold next. This morning energy prices are dropping again, with WTI crude down below $76.

Today we have the Purchasing Managers Indexes, or PMIs, from Markit IHS out at 0945. These are surveys of business owners (or those who do the purchasing at these companies). There are a bunch of different sectors that are surveyed. Economists mainly care about services, manufacturing, and the composite reading. Expectations are for these to have risen a bit, to around 59, well above the 50 level that separate expansion from contraction.

This is an important snapshot of how business managers are perceiving the economic situation. It is a survey, but it is seen as a forward-looking indicator. Obviously this being the U.S., the services reading is more important as this is a far larger part of the economy. The readings in Europe were just published this morning and mostly showed better than expected numbers.

We also have some earnings today, with American Eagle (AEO), Best Buy (BBY), Dollar Tree (DLTR), and Abercrombie & Fitch (ANF) before the open at 0930. Dell (DELL), Gap (GPS), HP (HPO), and Nordstrom (JWN) report after the close at 1600.

Bottom Line

With stocks and bonds selling off it is only a time before investors start putting the cash back to work. The only question is, where? If inflation concerns are paramount, then that would not make bonds a very good idea. But the party may be over for pandemic stocks, regardless of what happens with lockdowns.

Yesterday’s Bottom Line told you to watch for the Fed announcement and to keep an eye out for an upset pick. Well, one out of two isn’t bad. An announcement was made (before the open even) and Jerome Powell was re-appointed as Fed chair. Stocks initially rallied on the news, with the S&P and Nasdaq setting fresh intraday record highs, then declined. When all was said and done the Nasdaq dropped by 1.3% and S&P by 0.3%. Dow Industrials held on to gains, but barely.

Share this post