Good morning contrarians! And happy St. Patrick’s Day.

Stock futures are down a bit after another day of big gains on Wall Street. The Nasdaq was up almost 4% on the day with other indexes adding about 2%. It’s not entirely clear what caused this rally, which seemed to intensify as Fed chair Jay Powell was speaking. Earlier in the day came reports of Russia and Ukraine making progress in their peace talks. Apparently a 15-point plan would have Ukraine abandon any plans to join NATO in for security guarantees.

State of Play

Whatever the cause, stocks have pared their gains this morning. Asia closed higher but European indexes are now down a bit. Here in the U.S. indexes are due to open a little lower, judging by futures.

Commodities are rallying again, with WTI crude up 5% to trade near $100/barrel. Industrial commodities are up again, with palladium and aluminium up 4% and 6%, respectively. Precious metals are gaining as well, with gold, silver, and platinum up 2% to 4%. But nickel, which has resumed trading, promptly fell 8% to hit a new trading limit. Nickel prices more than doubled on March 8, causing the London Metal Exchange to suspend trading.

Bonds are continuing to sell off, with the 2-year yield now up 5 basis points to 1.92% and the 10-year up 7bps to 2.16%. Cryptos are flat with bitcoin stuck on $40,600.

The Fed

The FOMC did what was expected, which is announce an increase of 0.25% to its key rate. The Fed also penciled in rate hikes at each of its future meetings this year (so six in all) and said it would start the balance sheet run-off at “a coming meeting.” Powell in his remarks hinted this could be May. The Fed also pared its outlook for growth.

None of this sounds particularly dovish, so the rally is a bit mystifying. Perhaps it was Powell’s comments that the Fed would be “nimble” if the data changed or his assessment of “not particularly elevated” chances of a recession in the U.S. in the coming 12 months.

Economic Data

We just had Eurozone CPI come in a smidge higher than anticipated, printing at 5.9% year-over-year versus expectations of 5.8%. The core figure was exactly in line with estimates, 2.7% YoY.

The Bank of England decides on interest rates at 0800. The consensus expectation is for the BoE to raise its benchmark rate to 0.75% from 0.5%, so the same quarter-rate increase as the Fed announced yesterday. The BoE is ahead of the Fed though because the BoE started its interest-rate hiking at its last meeting a month ago with an initial 25 basis point increase.

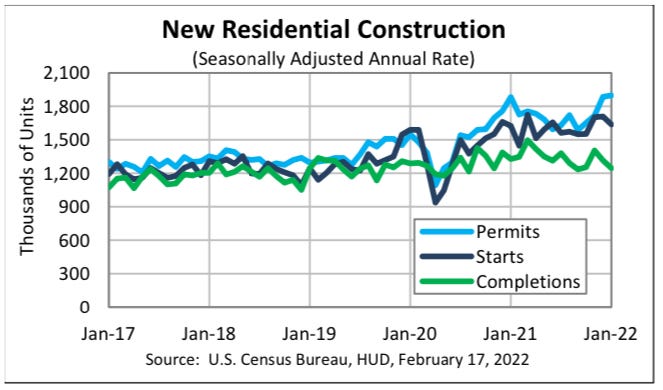

Then we have the U.S. census bureau release its new residential construction data for January, at 0830. This consists of a couple of metrics, the most important of which are building permits and housing starts. These are the leading indicators for the U.S. real estate market, which is very much the leading engine of global economic growth. If Americans are buying homes, it means they have cash and risk appetite, which means they will be buying other things besides homes (in addition to stuff to furnish these homes). This means factories in China and elsewhere can produce more stuff, which means they have to import more raw materials from commodities exporters. Seen this way, building permits and housing starts are one of the leading indicators for the global economy.

Economists expect 1.85 million new permits for February, down a bit from the 1.9 million seen in January. Housing starts for the month are expected to have increased a bit, to 1.69 million from 1.64 million. Last month saw both metrics come in at pretty low levels. There may have been a seasonal element for this, but it’s worth watching to see how it prints.

Seeing how it’s Thursday we will also have initial jobless claims out at the same time. Economists expect 220,000 new claims, down a bit from the 227,000 seen last week.

U.S. industrial and manufacturing production is out at 0915. The forecast here is for month-over-month increases of 0.5% and 0.6%, respectively. The year-over-year figure is probably more telling, but there is no survey for that one.

Earnings

Warby Parker (WRBY) and Dollar General (DG) report before the open at 0930. After the close at 1600 we’ll hear from FedEx (FDX) and GameStop (GME).

The Bottom Line

There’s a lot going on, but any uncertainty of Fed policy should be removed by now — until market forces lead Powell & Co. to change their hand again. The rally we’ve seen in stocks this week is a mystery to many. Maybe it is just short-covering, as our guest last week surmised.

One would think investors may be shrugging off Russia-Ukraine too quickly, only because these peace negotiations take time and involve many steps back as well as forward. Reports of progress are great, but the devil is in the details and the situation on the ground remains perilous.

One thing that’s certain is these events have forced humility on market prognosticators. A reminder of how important it is to keep the contrarian view in mind, even if one doesn’t always act on it.

Share this post